How I Stayed Calm When Disaster Hit — My Real Financial Backup Plan

What happens when life throws a curveball — a sudden job loss, a car crash, or a medical emergency? I learned the hard way that without a solid financial plan, one accident can unravel everything. A few years ago, I was caught off guard and nearly broke. But that moment changed me. I built a practical, no-nonsense system to protect myself — not with complex investments, but with smart, simple moves anyone can make. This is how I turned panic into peace.

The Moment Everything Changed

It started with a trip to the doctor that I thought would be routine. A persistent back pain turned out to be a herniated disc requiring physical therapy and months of limited mobility. At the time, I worked in a job that didn’t offer paid sick leave. Within weeks, my income dropped by 70 percent. Bills piled up — rent, utilities, car payments — and my savings, which I believed were adequate, vanished in less than two months. I remember sitting at my kitchen table, staring at a stack of overdue notices, feeling a knot of dread tighten in my chest. It wasn’t just the money — it was the helplessness, the loss of control. I had always considered myself responsible, but I realized I had been living on the edge without even knowing it.

This experience exposed the fragility of a life built solely on steady paychecks. I wasn’t alone. Millions of households operate with minimal financial cushion, assuming that as long as the income keeps flowing, everything is fine. But life rarely follows a predictable path. Job losses, health setbacks, home repairs — these aren’t rare events. They are statistically common, yet most people don’t prepare for them until it’s too late. The turning point for me wasn’t just the crisis itself, but the realization that financial security isn’t about how much you earn. It’s about how well you can withstand disruption. That shift in mindset — from earning to enduring — became the foundation of my new approach.

What made the situation worse was the emotional toll. Stress affected my sleep, my relationships, and even my ability to focus on recovery. I began to understand that financial instability doesn’t just threaten your bank account — it erodes your well-being. The pressure to make ends meet led to rushed decisions, like considering high-interest personal loans. But something inside me resisted. I started researching, reading, and talking to financial counselors. I discovered that while I couldn’t control the injury, I could control my response. And that response would shape my future. The journey to financial resilience began not with a windfall or a miracle, but with a decision: to build systems, not just save money.

Why Traditional Advice Falls Short

When I first looked for guidance, I kept hearing the same advice: “Save six months of expenses.” It sounded reasonable — until I did the math. My essential monthly expenses were around $3,500. Six months meant $21,000. At the time, I had less than $4,000 in savings. For someone living paycheck to paycheck, that goal felt impossible, even discouraging. The traditional model assumes stable income, no debt, and consistent savings capacity — conditions that don’t reflect the reality for many working families. When income fluctuates, or when unexpected costs arise monthly, the idea of setting aside hundreds of dollars every month becomes a fantasy.

Another flaw in conventional advice is its rigidity. It treats financial planning like a one-size-fits-all formula, ignoring differences in job security, family size, geographic cost of living, and existing obligations. For example, someone working part-time or as an independent contractor faces a different risk profile than a salaried employee. Yet the same “six-month rule” is applied universally. This disconnect between theory and reality leads many to give up before they even start. They feel like failures for not meeting a standard that wasn’t designed for their circumstances.

There’s also the myth of perfect budgeting. Many financial programs emphasize tracking every dollar, cutting every non-essential expense, and achieving a flawless spending plan. While discipline matters, life is too unpredictable for perfect control. A child gets sick, a car breaks down, or a utility bill spikes — and the carefully crafted budget collapses. Instead of helping, this all-or-nothing mindset often leads to guilt and abandonment of the entire effort. What I needed wasn’t perfection. I needed flexibility. I needed a system that could absorb shocks, not one that fell apart at the first sign of trouble.

What became clear was that real financial resilience isn’t about hitting arbitrary targets. It’s about creating layers of protection that adapt to different levels of crisis. It’s about progress, not perfection. And it’s about designing a plan that works for your life — not someone else’s idealized version of it. This understanding allowed me to move beyond guilt and start building something practical, something that could survive real-world pressures.

Building Your Financial Shock Absorbers

I began to think of financial protection not as a single emergency fund, but as a series of shock absorbers — each designed to handle a different level of impact. Just as a car has front and rear suspension to handle bumps and potholes, your finances need multiple layers to manage small setbacks and major disruptions. My system now has three tiers: immediate cash, mid-term reserves, and strategic backup resources. Each serves a distinct purpose and is funded in a way that doesn’t compromise long-term goals like retirement or homeownership.

The first layer is immediate-access cash — about $1,000 kept in a separate high-yield savings account. This isn’t for retirement or vacations. It’s strictly for true emergencies: a broken appliance, an unexpected medical co-pay, or a minor car repair. The key is accessibility. I don’t want to sell investments or wait for a loan approval when the water heater fails on a Sunday night. This fund is liquid, safe, and mentally off-limits for anything else. Setting it up was simple: I automated a $50 transfer each paycheck until I reached the target. It wasn’t fast, but it was consistent.

The second layer is my mid-term reserve — about three months of essential expenses, held in a combination of a high-yield savings account and a short-term certificate of deposit (CD) with a no-penalty withdrawal option. This covers larger disruptions like job loss or medical leave. Because I don’t need instant access, I can earn slightly higher interest while still maintaining flexibility. I fund this gradually, adjusting contributions based on my monthly cash flow. In good months, I add more. In tight months, I protect the minimum. The goal isn’t speed — it’s sustainability.

The third layer is less about cash and more about options. This includes a low-interest credit line I’ve pre-qualified for, a network of freelance opportunities I’ve tested, and a list of assets I could sell if absolutely necessary — like extra electronics or furniture. These aren’t first-line solutions, but they provide breathing room in extreme situations. Importantly, I’ve already done the research: I know the interest rate on the credit line, I’ve completed trial gigs on freelance platforms, and I’ve checked resale values. This preparation means I won’t make rash decisions under pressure. Together, these layers create a buffer that allows me to respond calmly, not react in panic.

Smart Risk Control: Insurance That Actually Makes Sense

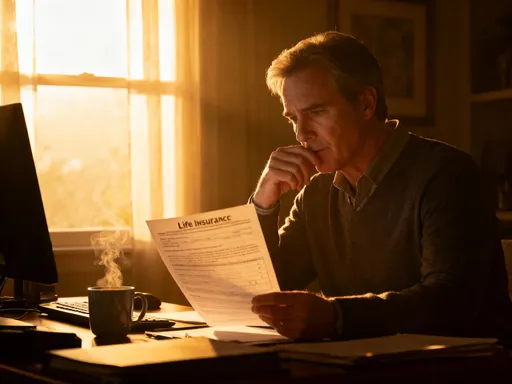

After my medical incident, I realized I had a dangerous gap in my coverage. My health insurance covered most of the treatment, but not the lost income. That’s when I discovered disability insurance — a type of protection that replaces a portion of your income if you’re unable to work due to illness or injury. It wasn’t something I had prioritized before, assuming I was healthy enough to skip it. But statistics show that one in four 20-year-olds will experience a disability before retirement. For someone relying on earned income, that’s a significant risk.

I reviewed my policies carefully, not just the coverage amounts but the fine print. Many standard plans have waiting periods, limited durations, or exclusions for pre-existing conditions. I switched to a provider that offered a 90-day waiting period with benefits lasting up to two years — a balance between affordability and protection. The monthly premium was about $65, a small price compared to the potential loss of thousands in income. I also made sure the policy was portable, so it wouldn’t vanish if I changed jobs.

Beyond health and disability, I evaluated my renters and auto insurance. I increased my liability coverage slightly, not because I expected lawsuits, but because legal costs can escalate quickly even from minor incidents. I also added roadside assistance to my auto policy — a small add-on that saved me $120 when my battery died last winter. These adjustments weren’t about fear-mongering. They were about closing gaps — identifying where a small investment could prevent a large loss.

Insurance isn’t a guarantee against hardship, but it’s a tool for managing risk. The key is to buy coverage that aligns with your actual vulnerabilities, not the ones marketers emphasize. I no longer see insurance as just another bill. I see it as part of my financial infrastructure — like brakes on a car. You don’t buy them because you plan to crash. You buy them because you value control and safety.

Income Backup Lines: What to Do When Paychecks Stop

One of the most frightening aspects of financial crisis is the sudden silence of the direct deposit. Without income, even a well-funded emergency account can drain quickly. That’s why I now treat income resilience as a core part of my financial plan. Before my health issue, I assumed that if I lost income, I’d figure it out later. But crisis is not the time to start building skills or searching for opportunities. That’s why I now maintain what I call “income backup lines” — pre-vetted ways to earn money if my primary source dries up.

I started by identifying my transferable skills. I have experience in writing, data entry, and basic graphic design. I created simple profiles on reputable freelance platforms and completed a few small projects — not for the money, but to build ratings and confidence. I also reached out to local businesses to offer part-time help with social media or bookkeeping. These weren’t full-time jobs, but they proved I could generate income quickly if needed.

I also explored passive options, like renting out a spare room through a short-term rental platform. I prepared the space, took photos, and created a listing — all before I needed it. When I briefly hosted a traveling nurse for three weeks, I earned enough to cover my car payment. The experience showed me that having options isn’t about desperation — it’s about freedom. It means I’m not trapped by a single income stream.

The most important lesson was testing these options in advance. I didn’t wait for a crisis to see if they worked. I treated them like fire drills — practicing so I wouldn’t panic when the alarm sounded. Now, if my income were interrupted, I wouldn’t start from zero. I’d have a map, a plan, and the confidence that I could keep moving forward.

Avoiding the Common Traps That Wreck Finances

In the early days of my crisis, I came close to making a decision I would have regretted: withdrawing $8,000 from my retirement account. A financial advisor warned me about the 10 percent penalty and income tax, but I was desperate. What stopped me was a simple question: “How will you feel about this in two years?” I realized I was trading long-term security for short-term relief — a pattern I’ve seen repeated in many financial downfalls. People raid retirement savings, max out credit cards, or take payday loans, not because they’re careless, but because they’re overwhelmed.

These emotional decisions often lead to long-term damage. Withdrawing from retirement accounts not only triggers penalties but also loses years of compound growth. Maxing out credit cards can lead to debt cycles that take years to escape. Payday loans, with their triple-digit interest rates, can trap borrowers in a spiral of repayment. These are not solutions — they are financial quicksand.

What helped me avoid these traps was having a clear hierarchy of resources. I decided in advance what to use and in what order: first, my emergency fund; second, my mid-term reserve; third, low-interest credit; and only as a last resort, selling assets. I also set personal rules, like never touching retirement funds for non-retirement expenses. These boundaries gave me structure when emotions ran high.

I also reached out for help. I contacted my lenders to request payment plans. I used community resources for temporary utility assistance. I learned that asking for help isn’t weakness — it’s strategy. By avoiding the common traps, I protected my future. The crisis was hard, but it didn’t define my financial life. I emerged with scars, but also with wisdom.

Putting It All Together: A Realistic, Flexible Plan

Building a financial safety net doesn’t require a high income or financial genius. It requires intention, consistency, and a willingness to adapt. My plan isn’t perfect. There are months when I can’t add to my reserves, and times when I dip into the emergency fund. But the system holds. It bends instead of breaks. The key has been to focus on progress, not perfection. I started small — $20 a week — and built from there. I prioritized based on my reality: debt, income stability, and family needs.

I began by listing my vulnerabilities: no paid sick leave, high medical deductible, single income. Then I matched each with a solution: disability insurance, emergency fund, income backup lines. I didn’t try to fix everything at once. I tackled one layer at a time, celebrating small wins. Each step gave me more confidence and control.

I also adjusted my mindset. I stopped seeing financial planning as a burden and started seeing it as self-care. Just as I eat well and exercise to protect my health, I save and prepare to protect my peace of mind. This shift made the process sustainable. I no longer feel deprived when I transfer money to savings. I feel empowered.

Today, I still face challenges. Inflation, rising costs, and economic uncertainty are real. But I no longer feel helpless. I have a plan that adapts. I review it twice a year, updating my income backup options, checking insurance coverage, and adjusting savings goals. It’s a living system — not a rigid rulebook. And that flexibility is what makes it work.

True financial strength isn’t measured by wealth — it’s revealed in how you handle the unexpected. A crisis doesn’t have to mean collapse. With practical planning, clear thinking, and a few smart moves, you can build a life that bends instead of breaks. This isn’t about fear — it’s about freedom. And that peace of mind? Totally worth it.